Labour’s pledge to reintroduce the 50p tax rate for those on incomes of over £150,000 a year has met with a hostile business press. Mind you, as it is mainly the captains of industry, investment bankers and senior partners in legal and accounting firms who will be paying it, that’s not perhaps surprising.

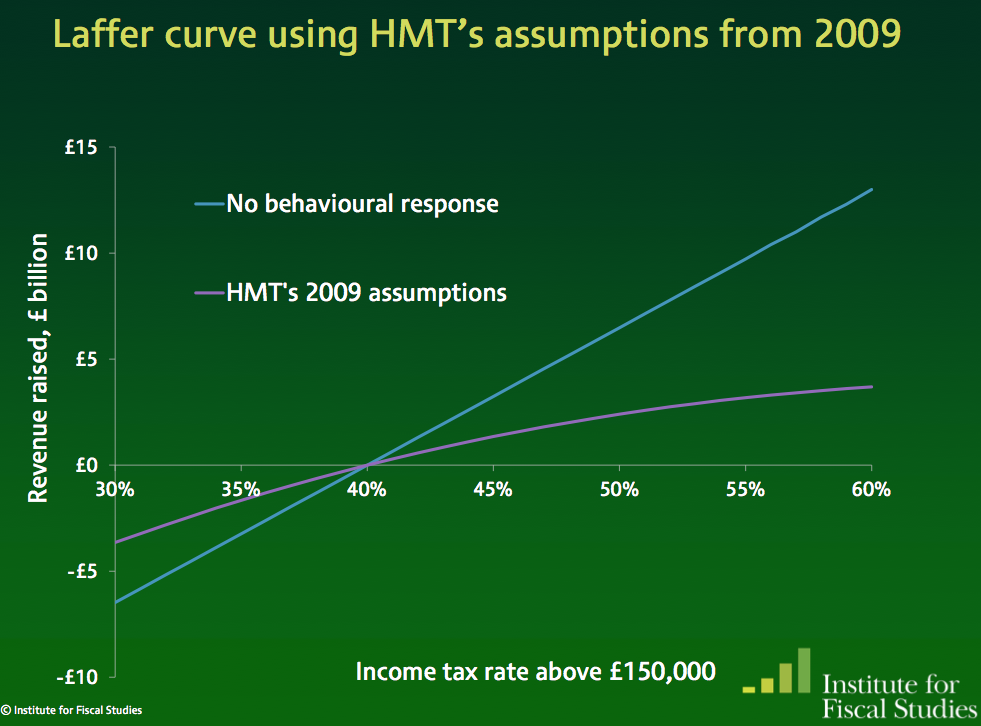

What has surprised me, as I have read into some of the background policy analysis, is how difficult it is to estimate the impact on the deficit. What HMRC calls the “static costing” is straightforward enough – reducing the rate, in 2012 from 50p to 45p was estimated to cost £3bn or so. But the net effect depends on how successful top rate taxpayers would be in shifting income otherwise liable to the 50p rate elsewhere – to another year, to another country, or to a form of income taxed less highly – say dividends or (even better) capital gains. HMRC ‘s exhaustive (and exhausting) analysis reckoned this would reduce the net cost from £3bn to roughly £100m in a full year – a staggering level of behavioural response (see diagram above, from IFS). Indeed, hidden in the small print of the HMRC analysis is the giveaway sentence:

“the estimated revenue-maximising rate of tax for those with incomes over £150,000 is between 45 per cent and 50 per cent”

– in other words, at some point between a 45p tax rate and a 50p rate, an increase will actually reduce the tax tax. So, if you are going to “tax the rich till the pips squeak”, you had better stop somewhere between 45 and 50p.

Now in many countries the response would be “well, that’s what the Tories have paid HMRC to say”. But having waded through the document, I can confirm that, in this instance at least, the Northcote/Trevelyan reforms are holding good and it seems a pukka piece of analysis.

Labour’s problem is that there are just too many distortions in the tax system and too many opportunities for wealthy individuals to legally avoid tax. Part of this is related to globalisation – but part is the differential rates of tax in the UK between taxes on employment income and taxes on being self-employed or on dividends from a small business. Plus what are still generous treatments of capital gains versus earned income – differences which Venture Capital Trust allowances and their like amplify.

It is interesting that, while the 50p debate has been going on in the UK, across in Germany the Bundesbank was suggesting a wealth tax/capital levy could be a helpful device for countries [think Italy] seeking to reduce their deficits (see http://goo.gl/9BlQeB for the FT summary). Labour might find it more worthwhile, if less electorally popular, to delve into the mechanics of why so much income can be shifted in the UK, the taxation of wealth, and how, in a globalised world, “the rich” can be encouraged to pay “their fair share”.

Leave a comment